|

| Global Consumer Confidence Ranking. Source: Nielsen |

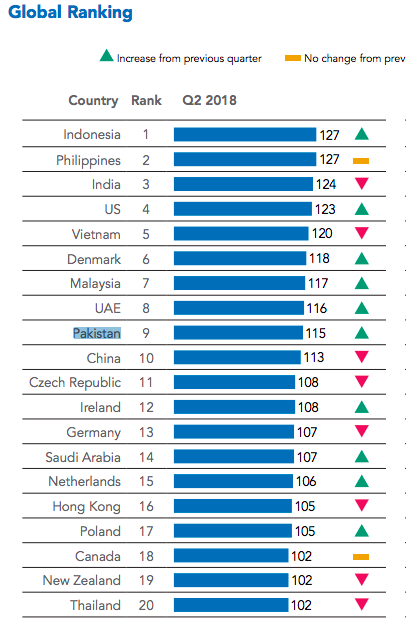

Here's an excerpt of the TCB-Global report on Pakistan:

"In Pakistan, consumer confidence has reached an all-time high of 115, following an 8-point increase. Consumers in Pakistan are increasingly optimistic about job prospects and their personal financial situation. However, it is uncertain whether the high level of confidence can be sustained in the future. Pakistan’s new government is likely to approach IMF for assistance to address the country’s worsening external balance, which might lead to significant fiscal and monetary tightening. This, along with rising consumer prices, will pose major challenges to consumer confidence post-election."

The survey indicates that Pakistan's domestic economy remains strong in spite of the rising concerns about balance of payments. The new Pakistani government headed by PTI leader Imran Khan is reporting some successes in alleviating these concerns with help from Islamabad's friends in Beijing and Riyadh. Saudi Arabia has already pledged $6 billion in cash and deferred oil payments. Since returning from a trip to Beijing, Pakistan's Finance Minister Asad Umar has said "Pakistan's immediate balance of payment crisis is over". It's highly likely that Pakistan will seek yet another IMF bailout with conditions that will force spending cuts and cause economy to slow down this year. This will hurt consumer confidence.

Related Links:

Haq's Musings

South Asia Investor Review

Can Pakistan Avoid IMF Bailouts?

Can Imran Khan Lead Pakistan to the Next Level?

Upwardly Mobile Pakistan

Pakistani Universities Among Asia's Best

Fear, Uncertainty and Doubt (FUD) About CPEC

South Asia Investor Review

Can Pakistan Avoid IMF Bailouts?

Can Imran Khan Lead Pakistan to the Next Level?

Upwardly Mobile Pakistan

Pakistani Universities Among Asia's Best

Fear, Uncertainty and Doubt (FUD) About CPEC

8 comments:

#Pakistan turns bullish with backing of #Beijing and #Riyadh. #Islamabad begins bailout talks with #IMF, but lacks sense of urgency. #China #SaudiArabia #CPEC

https://asia.nikkei.com/Economy/Pakistan-turns-bullish-with-backing-of-Beijing-and-Riyadh

Pakistan began negotiations with the International Monetary Fund this week on a bailout package, but the South Asian country feels no sense of urgency as it sees enough support from China and Saudi Arabia to avert a crisis, at least for now.

When Pakistan's main stock index -- the KSE-100 -- fell roughly 0.5% on Thursday, investors and analysts were hardly alarmed.

"A few weeks ago, investors were getting a heart attack every time the market sunk," a wealthy Pakistani equity investor said. "But today, many of us see hope in the future. No one is in a state of panic."

Shuja Rizvi, a stock market analyst in the southern port city of Karachi, said Pakistan's crisis is widely seen to have ended.

"People in the [stock] market are now much more relaxed," Rizvi said.

Senior cabinet ministers in Islamabad share that sense of returning comfort. Ahead of the beginning of formal talks between an IMF delegation and Pakistan on Wednesday, Finance Minister Asad Umar claimed that "Pakistan's immediate balance of payments crisis is over."

His comments came after Saudi Arabia last month announced a $6 billion loan to Pakistan -- half of that amount to boost the country's foreign currency reserves, and the other half in credits to finance part of the bill for oil imports during the current financial year ending in June 2019.

New Prime Minister Imran Khan visited China this month and met with government leaders. It was Khan's first visit to China since being elected as prime minister in July.

Though China did not announce an aid package like Saudi Arabia, senior Pakistaniofficials have told the Nikkei Asian Review that Beijing will continue to help Pakistan as it did in the last financial year. Chinese commercial banks lent at least $4.5 billion to boost Pakistan's liquid foreign exchange reserves last year -- a gesture that helped to avert an all-out default on foreign payments.

One senior finance ministry official on Thursday said that China was committed to protecting its interests, driven by a promised investment of $62 billion under the China-Pakistan Economic Corridor -- a cornerstone of Chinese President Xi Jinping's Belt and Road Initiative.

"China's interests in Pakistan are huge," the official added. "They [China] will quietly continue to help Pakistan to avoid an economic crisis."

But critics have warned that an end to the sense of crisis is not sufficient to stabilize Pakistan's economy for the medium to long term. The country's recurring challenges have included a failure to reform one of the world's worst-performing tax collection systems. Fewer than 1% of Pakistan's roughly 200 million people pay a regular income tax.

Additionally, the current-account deficit of about $18 billion during the last financial year -- Pakistan's largest ever -- was fueled by a failure to curb rising imports while exports crashed.

"Pakistan's industrial production has sagged over the years while the country's imports have grown and no credible reforms have taken place," said one Western economist in Islamabad who requested anonymity.

Pakistan still needs a loan from the IMF despite the greater comfort level among government decision makers, analysts said.

Overseas #Pakistanis remit $7.4 billion in first 4 months of FY19. During October 2018, the inflow of worker’s #remittances amounted to $2,000.47 million, which is 37.7% higher than September 2018 and 20.9% higher than October 2017. #CAD #IMF #Pakistan https://www.thenews.com.pk/latest/391754-overseas-pakistanis-remit-74-billion-in-first-four-months-of-fy19

Overseas Pakistani workers remitted $7419.98 million in the first four months (July to October) of FY19, compared with $6,444.46 million received during the same period in the preceding year.

During October 2018, the inflow of worker’s remittances amounted to $2000.47 million, which is 37.7% higher than September 2018 and 20.9% higher than October 2017.

The country wise details for the month of October 2018 show that inflows from Saudi Arabia, UAE, USA, UK, GCC countries (including Bahrain, Kuwait, Qatar and Oman) and EU countries amounted to $494.53 million, $412 million, $308.78 million, $298.80 million, $198.30 million and $57.36 million respectively compared with the inflow of $461.07 million, $333.57 million, $215.64 million, $270.46 million, $184.76 million and $51.12 million respectively in October 2017.

Remittances received from Malaysia, Norway, Switzerland, Australia, Canada, Japan and other countries during October 2018 amounted to $230.68 million together as against $137.83 million received in October 2017.

Without the remittances Pakistan would have a massive current account deficit more than double the actual deficit which is high enough. This is due to no real growth in exports over the last 8 years, a consequence of two civilian governments keeping the exchange rate greatly overvalued and the lack of reliable electricity for factories. The PKR has finally been allowed to fall to fair value, and this will allow export growth to resume, IMO the government needs to keep the PKR somewhat undervalued. This will make exports cheaper and suppress imports and will bring the current account deficit back down. CPEC has done much to reduce the electric power deficit. East Asia developed on the backs of undervalued currencies, Pakistan needs to replicate that.

These stats you bring up would be very heartening if Pakistan's economy was not strangulated by many structural issues. Lower savings rate, higher debt burden, poor tax collections and a general mis-allocation of resources.

One striking example is the quality of infrastructure amid the massive CPEC outlays. For example, take a simple metric - quality of roads. Pakistan was ranked 72 (India 90) in 2010, but in 2018 Pakistan slipped to 76 whereas India jumped to 56! It appears all eggs are in the CPEC basket, which may be fine, but not at the expense of other much needed issues.

- Munir Khan

MK: "These stats you bring up would be very heartening if Pakistan's economy was not strangulated by many structural issues"

A large population with high consumer confidence represents a big opportunity for serious investors. It's something that must be highlighted by Pakistan's leaders pitching to local and global investors. Increased investments in Pakistan will solve many of the problems you rightly bring up.

Munir Khan "One striking example is the quality of infrastructure amid the massive CPEC outlays. For example, take a simple metric - quality of roads. Pakistan was ranked 72 (India 90) in 2010, but in 2018 Pakistan slipped to 76 whereas India jumped to 56! It appears all eggs are in the CPEC basket, which may be fine, but not at the expense of other much needed issues."

Measures of the quality of roads as provided by the World Economic Forum are subjective; as the World Economic Forum itself says on the methodology of its report on this matter:

The Road quality indicator is one of the components of the Global Competitiveness Index published annually by the World Economic Forum (WEF). It represents an assessment of the quality of roads in a given country based on data from the WEF Executive Opinion Survey, a long-running and extensive survey tapping the opinions of over 14,000 business leaders in 144 countries. The road quality indicator score is based on only one question. The respondents are asked to rate the roads in their country of operation on a scale from 1 (underdeveloped) to 7 (extensive and efficient by international standards). The individual responses are aggregated to produce a country score.

So, individual "business leaders", opining on the quality of roads in their country in an anecdotal manner, entirely dependent on what they think are "international standards", is what this report "measures"; this is no independent study of the actual quality of roads done by, say, infrastructure professionals, in a scientific manner. It can lead to remarkable absurdities. In the 2016-17 rankings, India's quality of roads was rated as better than Kuwait's or Norway's quality of roads!

Or how about this: the UK's roads were rated as worse than those of Namibia or Ecuador! Where I live in the UK, this has lead to alarmist articles in newspapers along the lines of how the UK has worse roads than developing countries in Africa or Latin America, because such news items are devoid of the context of how these rankings are compiled.

See for yourself:

Here is a link to 2016-17 rankings on the World Economic Forum's website: http://reports.weforum.org/pdf/gci-2016-2017-scorecard/WEF_GCI_2016_2017_Scorecard_EOSQ057.pdf

And an example of the sort of news story in the UK that I had mentioned based on the above "shocking" report (with no mention of the report's methodology): https://www.standard.co.uk/news/transport/britains-roads-are-worse-than-in-some-poorer-countries-shocking-report-reveals-a3472861.html

If one wishes to rely on anecdotal impressions when comparing road quality in India and Pakistan, those who have some knowledge of both have tended, even in very recent years, to regard Pakistan as doing better on this score, especially when it comes to rural road networks. Similarly, India is regarded as having a better quality of railways. Needless to say, a more scientific assessment is obviously superior to any such set of observations.

With regard to CPEC and infrastructure, most mainstream analysts who are actually in the know of CPEC's details, and do not have an axe to grind in the way that certain parts of the US media/establishment does (e.g., the Wall Street Journal in its pieces on CPEC), or pretty much the entirety of India's political and media opinion does, see CPEC as being a undoubted boon for Pakistan's transport infrastructure.

According to the State Bank of Pakistan (SBP), adverse movement in global oil prices, coupled with strong demand for industrial raw materials – metals and allied products – was mainly responsible for the higher imports. Resultantly, the country’s balance of payments came under severe strain during the past year.

In FY18, Pakistan witnessed a record trade deficit of US$ 37.6 billion; 15.7 percent higher from last year. The broad-based and quantumled rebound in exports – after consecutive declines over the last three years – was overshadowed by surging imports, which almost touched the US$ 61.0 billion mark.

However, the overall exports in first four months of FY19 increased by 3.52 percent to $7.38 billion as compared to $ 7.13 billion worth of goods exported in corresponding period of previous fiscal year. Imports in first four months of FY19 remained intact, going up by 0.06 percent to $ 19.17 billion as against $ 19.16 billion in the same period of FY18.

Pakistan’s trade account is showing early signs of improvement under the spirit of the new economic policy as country’s trade deficit in first four months of current fiscal fell to $ -11.8 billion from the $ -12.1 billion reported in corresponding period of last fiscal, official data showed on Monday.

https://dailytimes.com.pk/321451/pakistans-trade-balance-improving-as-exports-continue-to-grow/

Good inputs there. Indeed the quality of roads measured is a hit and miss when it comes to WEF surveys. The same has been taken into cognizance by Frontier Works Organization which will work with WEF to update progress on various improvements undertaken by them. Ranking for Pakistan will go up considerably next year.

Post a Comment