Growing access to smartphones and Internet connectivity is transforming the lives of women in rural Pakistan. They are acquiring knowledge, accessing healthcare and finding economic opportunities. A recent UNDP report titled "DigitAll: What happens when women of Pakistan get access to digital and tech tools? A lot!" written by Javeria Masood describes the socioeconomic impact of technology in Pakistan in the following words:

"The world as we know it has been and is rapidly changing. Technology has proven to be one of the biggest enablers of change. There has been a significant emphasis on digital trainings, tech education, and freelancing in the last several years especially during the pandemic, through initiatives from the government, private and development sectors. Covid-19 acted as a big disrupter and accelerated the digital uptake many folds. In Pakistan, we saw the highest number of digital wallets, online services, internet-based services and adaptability out of need and demand".

|

| Pakistani Women in South Punjab. Photo by Shuja Hakim UNDP Pakistan |

Digital Transformation:

The report cites the example of Ayesha Abushakoor from Zawar Wala in South Punjab who is a Quran teacher. She is teaching students remotely in and outside Pakistan. She uses digital wallets to receive payments. The same report also cites the case of Samina, from Muzafargharh, who is getting training online to start a livestock business. Another woman Mujahida Perveen from UC Pega in Dera Ghazi Khan is managing her thyroid disease by watching YouTube videos.

Telehealth is helping more women access healthcare in remote areas of Pakistan. Startups like Sehat Kahani are employing women doctors who work from home to provide healthcare services. Sehat Kahani was founded by Dr. Sara Khurram and Dr. Iffat Zafar who raised seed funding of US$ 500,000 in 2018, followed by a pre-series of $1 million in March 2021.

Expansion of Digital Services:

The year 2022 was a very rough year for Pakistan. The nation was hit by devastating floods that badly affected tens of millions of people. Macroeconomic indicators took a nose dive as political instability reached new heights. In the middle of such bad news, Pakistan saw installation of thousands of kilometers of new fiber optic cable, inauguration of a new high bandwidth PEACE submarine cable connecting Karachi with Africa and Europe, and millions of new broadband subscriptions. Broadband penetration among 140 million (59% of 236 million population) Pakistanis in the 15-64 years age group reached almost 90%. This new digital infrastructure helped grow technology adoption in the country.

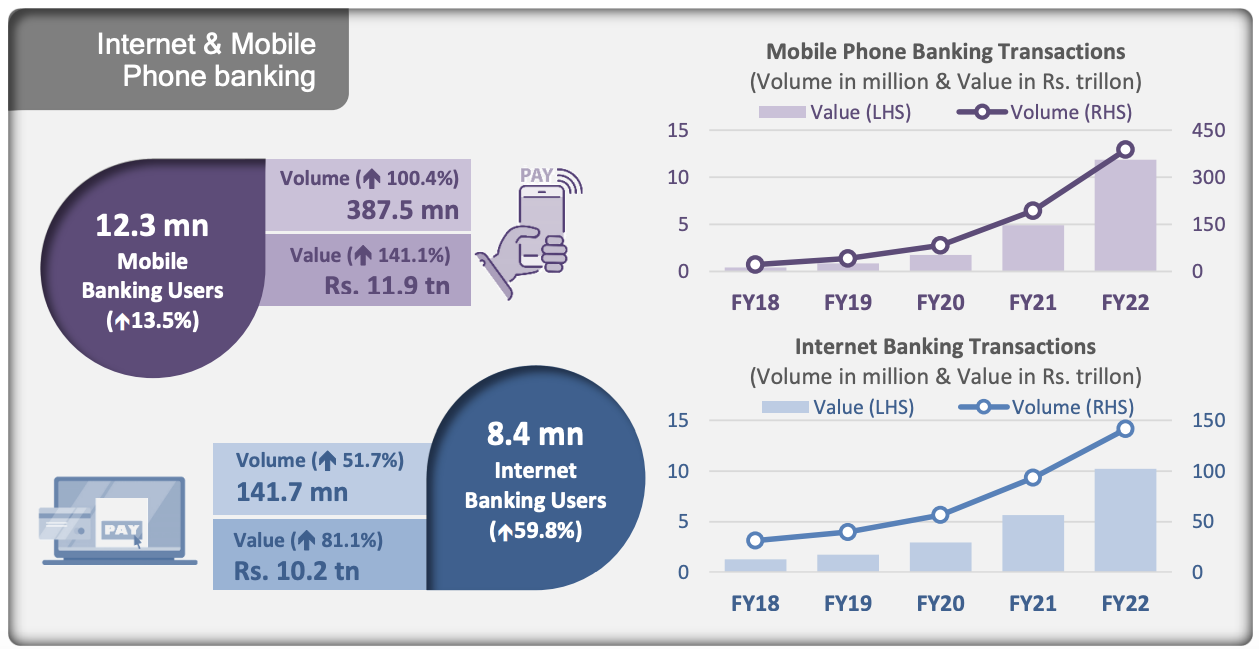

|

| Internet and Mobile Phone Banking Growth in 2021-22. Source: State Bank of Pakistan |

Fintech:

Mobile phone banking and internet banking grew by 141.1% to Rs. 11.9 trillion while Internet banking jumped 81.1% to reach Rs10.2 trillion. E-commerce transactions also accelerated, witnessing similar trends as the volume grew by 107.4% to 45.5 million and the value by 74.9% to Rs106 billion, according to the State Bank of Pakistan.

|

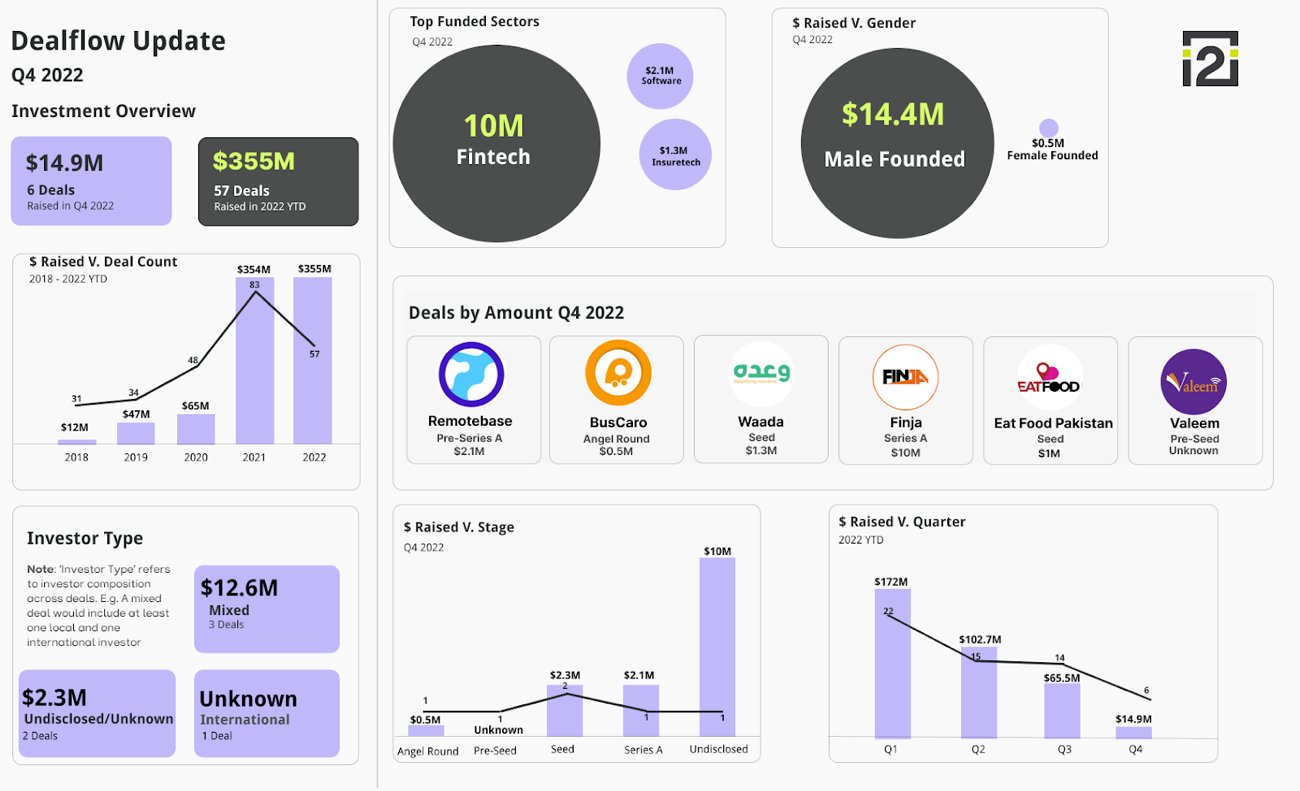

| Pakistan Startup Funding in 2022. Source: i2i Investing |

Fintech startups continued to draw investments in the midst of a slump in venture funding in Pakistan. Fintech took $10 million from a total of $13.5 million raised by tech startups in the fourth quarter of 2022, according to the data of Invest2Innovate (i2i), a startups consultancy firm. In Q3 of 2022, six out of the 14 deals were fintech startups, compared to two deals of e-commerce startups. Fintech startups raised $38 million which is 58% of total funding ($65 million) in Q3 2022, compared to e-commerce startups that raised 19% of total funding. The i2i data shows that in Q3 2022, fintech raised 37.1% higher than what it raised in Q2 2022 ($27.7 million). Similarly, in Q2 2022, the total investment of fintech was 63% higher compared to what it raised in Q1 2022 ($17 million).

|

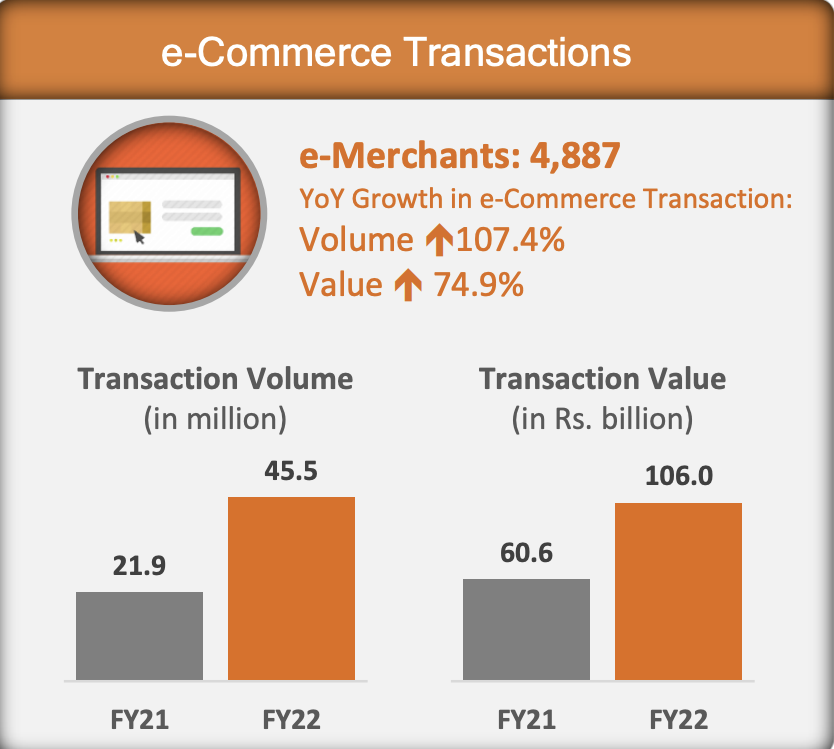

| E-Commerce in Pakistan. Source: State Bank of Pakistan |

E-Commerce:

E-commerce continued to grow in the country. Transaction volume soared 107.4% to 45.5 million while the value of transactions jumped 75% to Rs. 106 billion over the prior year, according to the State Bank of Pakistan.

|

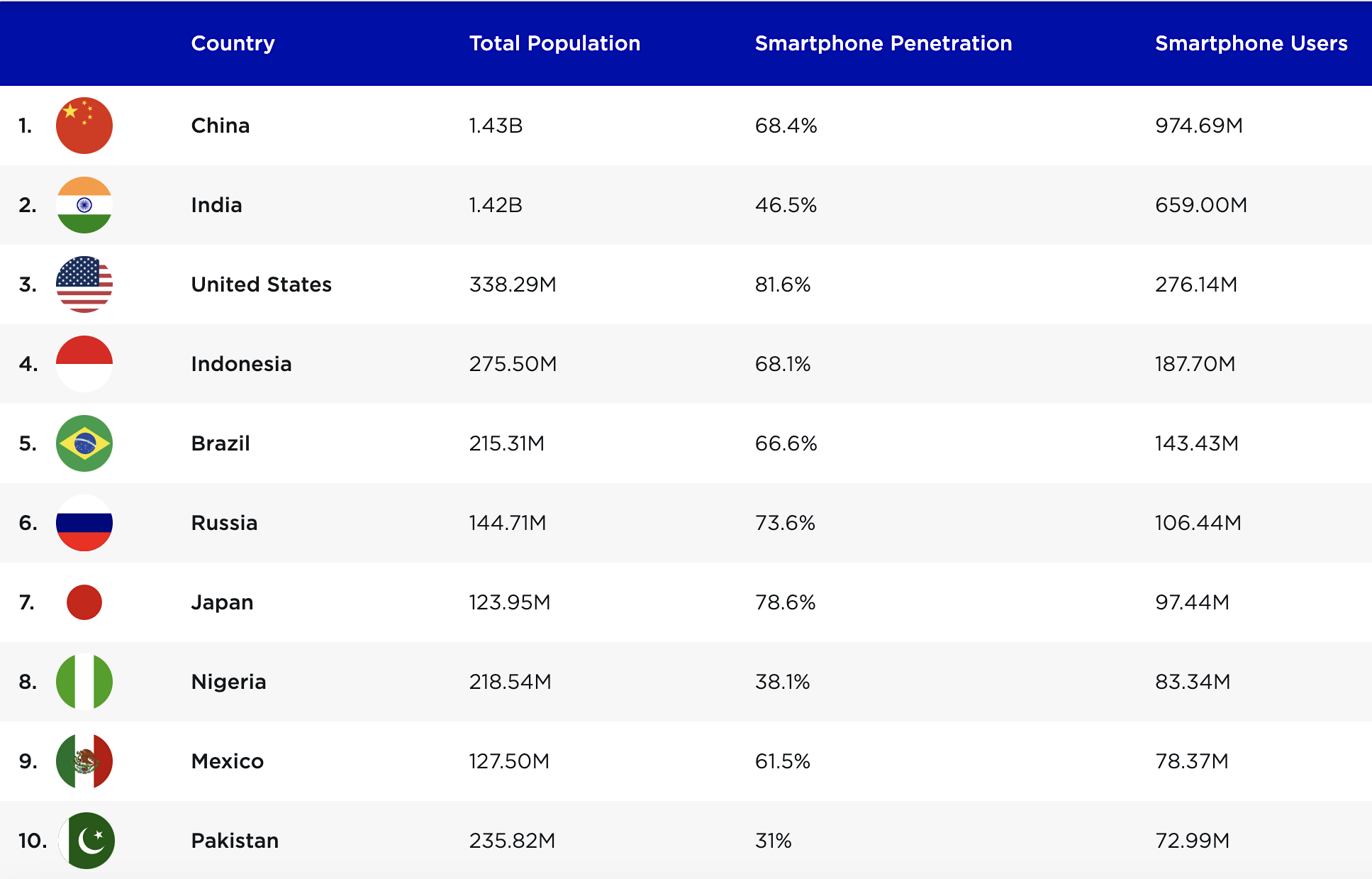

| Pakistan Among World's Top 10 Smartphone Markets. Source: NewZoo |

PEACE Cable:

Pakistan and East Africa Connecting Europe (PEACE) cable, a 96 TBPS (terabits per second), 15,000 km long submarine cable, went live in 2022. It brought to 10 the total number of submarine cables currently connecting or planned to connect Pakistan with the world: TransWorld1, Africa1 (2023), 2Africa (2023), AAE1, PEACE, SeaMeWe3, SeaMeWe4, SeaMeWe5, SeaMeWe6 (2025) and IMEWE. PEACE cable has two landing stations in Pakistan: Karachi and Gwadar. SeaMeWe stands for Southeast Asia Middle East Western Europe, while IMEWE is India Middle East Western Europe and AAE1 Asia Africa Europe 1.

|

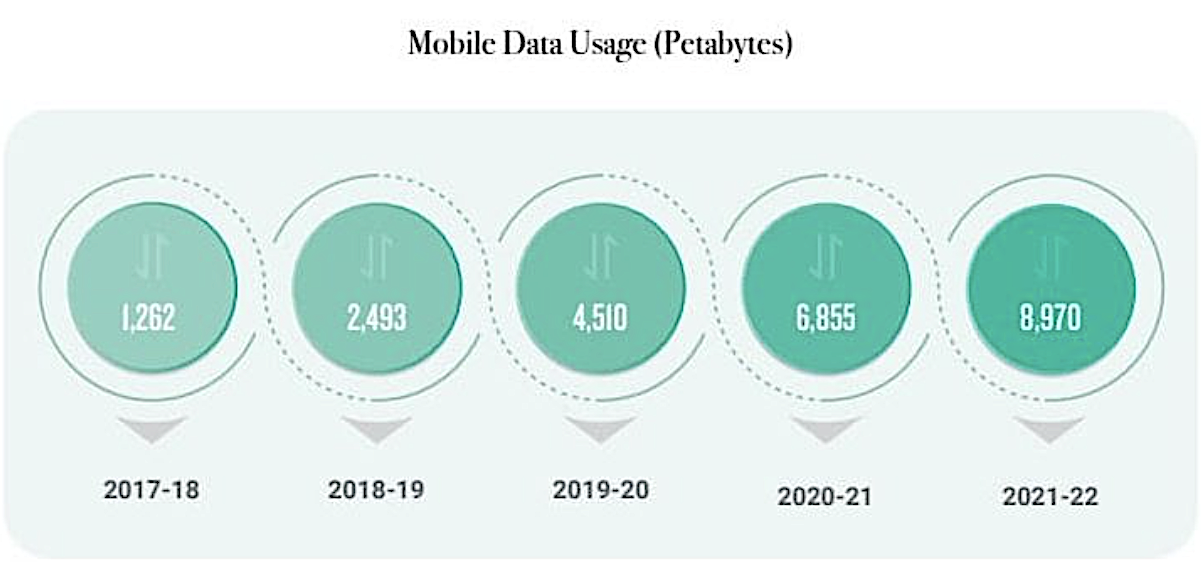

| Mobile Data Consumption Growth in Pakistan. Source: ProPakistan |

Fiber Optic Cable:

The first phase of a new high bandwidth long-haul fiber network has been completed jointly by One Network, the largest ICT and Intelligent Traffic and Electronic Tolling System operator in Pakistan, and Cybernet, a leading fiber broadband provider. The joint venture has deployed 1,800 km of fiber network along motorways and road sections linking Karachi to Hyderabad (M-9 Motorway), Multan to Sukkur (M-5 Motorway), Abdul Hakeem to Lahore (M-3 Motorway), Swat Expressway (M-16), Lahore to Islamabad (M-2 Motorway) and separately from Lahore to Sialkot (M-11 Motorway), Gujranwala, Daska and Wazirabad, according to Business Recorder newspaper.

Mobile telecom service operator Jazz and Chinese equipment manufacturer Huawei have commercially deployed FDD (Frequency Division Duplexing) Massive MIMO (Multiple Input and Output) solution based on 5G technology on a large scale in Pakistan. Jazz and Huawei claim it represents a leap into the 4.9G domain to boost bandwidth.

|

| Pakistan Telecom Indicators November 2022. Source: PTA |

|

| Pakistan's RAAST P2P System Taking Off. Source: State Bank of Pakistan |

Broadband Subscriptions:

Pakistan has 124 million broadband subscribers as of November, 2022, according to Pakistan Telecommunications Authority. Broadband penetration among 140 million (59% of 236 million) Pakistanis in 15-64 years age bracket is 89%. Over 20 million mobile phones were locally manufactured/assembled in the country in the first 11 months of the year.

|

| Bank Account Ownership in Pakistan. Source: Karandaaz |

|

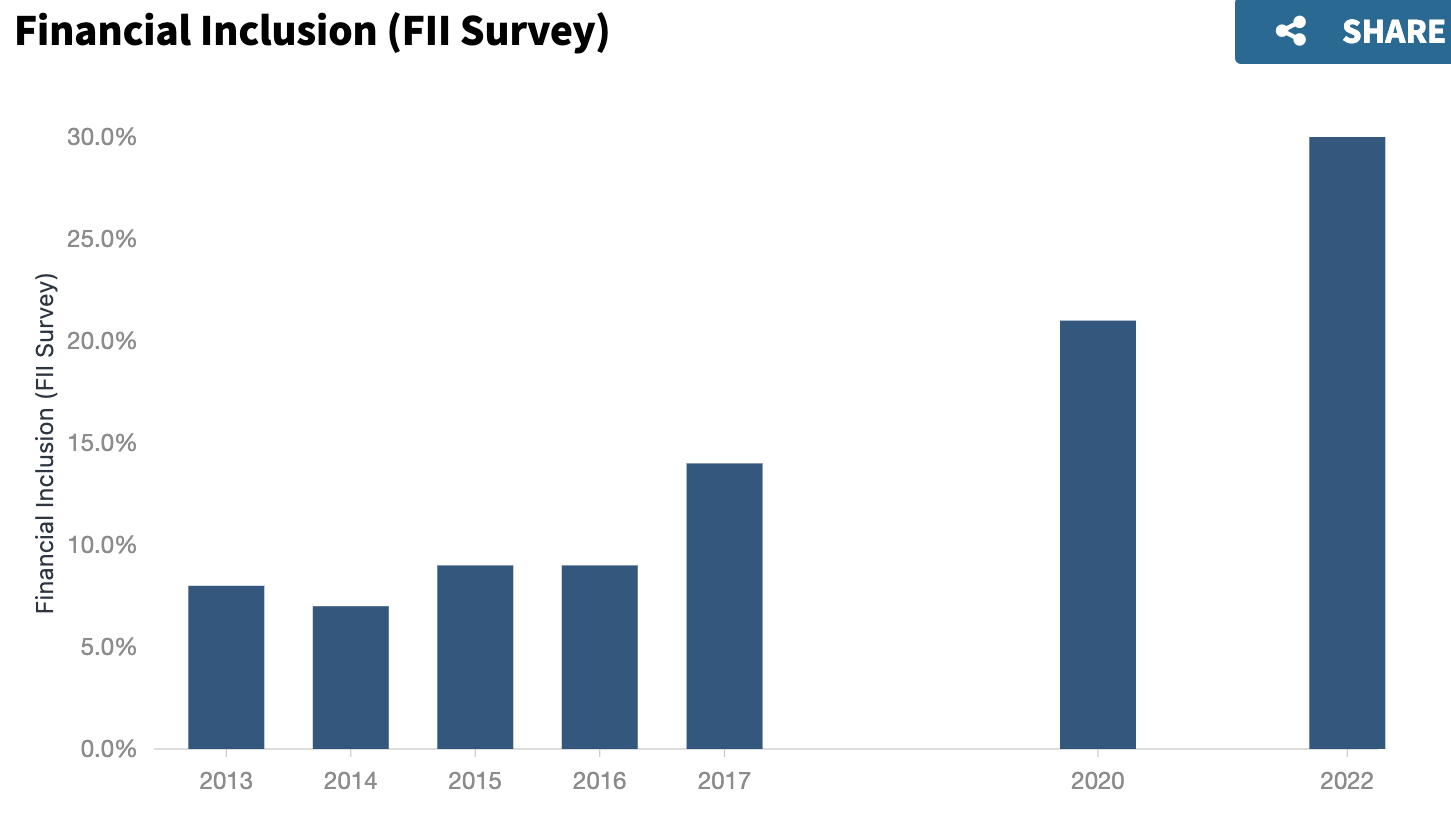

| Financial Inclusion Doubled In Pakistan in 5 Years. Source: Karandaaz |

Documenting Pakistan Economy:

Pakistan's unbanked population is huge, estimated at 100 million adults, mostly women. Its undocumented economy is among the world's largest, estimated at 35.6% which represents approximately $542 billion at GDP PPP levels, according to World Economics. The nation's tax to GDP ratio (9.2%) and formal savings rates (12.72%) are among the lowest. The process of digitizing the economy could help reduce the undocumented economy and increase tax collection and formal savings and investment in more productive sectors such as export-oriented manufacturing and services. Higher investment in more productive sectors could lead to faster economic growth and larger export earnings. None of this can be achieved without some semblance of political stability.

Related Links:

2021: A Banner Year For Tech Startups in Pakistan

Pakistan Projected to Be World's 6th Largest Economy By 2075

Digital Pakistan 2022: Broadband Penetration Soars to 90% of 15+ Population

Working Women Seeding a Silent Revolution in Pakistan

Socioeconomic Impact of New Infrastructure in Rural Pakistan

Pakistan Gets First Woman Supreme Court Judge

Pakistan at 75

Growing Presence of Pakistani Women in Science and Technology

Riaz Haq's Youtube Channel

35 comments:

#Pakistan’s Abhi Issues First #Sukuk #Bond for a #Fintech in Region. #Karachi-based startup raised 2 billion rupees ($6.8 million). Demand exceeded expectations with subscriptions reaching twice the anticipated amount. #startup #technology

https://www.bloomberg.com/news/articles/2023-05-12/pakistan-s-abhi-issues-first-sukuk-bond-for-a-fintech-in-region#xj4y7vzkg

Pakistan’s financial platform Abhi has raised the first-ever Sukuk bond for a fintech firm in the region, opening a new funding line for startups that have seen a slowdown in venture capital.

The Karachi-based startup raised 2 billion rupees ($6.8 million), an industry first for the Middle East, Africa and Pakistan region, said Omair Ansari, chief executive officer and co-founder. Demand exceeded expectations with subscriptions reaching twice the anticipated amount, he said in an interview.

Pakistan imposes widespread internet and social media bans • The Register

Outage-watching org NetBlocks has analyzed the performance of Pakistan's networks in recent days and substantiated reports of outages.

"NetBlocks metrics confirm the disruption of Twitter, Facebook and YouTube on multiple internet providers in Pakistan on Tuesday 9 May 2023. Additionally, total internet shutdowns have been observed on mobile networks in some regions," the outfit stated.

Digital rights advocacy organization Access Now has called for connectivity to be restored.

"People rely on the internet to obtain healthcare, education, and even earn their livelihoods," said the org’s Asia-Pacific policy director Raman Jit Singh Chima. "Hitting the kill switch is neither necessary nor proportionate, and can never be justified. Pakistani authorities must scrap their go-to tool used to quash political protests over the last year."

Chima's point about livelihoods applies to Pakistan itself: the nation promotes the use of freelance remote work platforms as a way for residents to earn a living and to improve services exports.

This round of lockdowns has, however, seen prominent freelance platform Fiverr warn users that workers in the nation are at risk, per the screenshot below.

Pakistan's financial gender gap aggravates chronic poverty

https://asia.nikkei.com/Spotlight/The-Big-Story/Pakistan-s-financial-gender-gap-aggravates-chronic-poverty

This week's Big Story examines Pakistan's financial gender gap. According to the World Bank's Global Findex Database, which tracks the use of financial services, only 13% of Pakistani women have their own bank accounts, compared with 28% of men. The story takes an in-depth look at what is still keeping women away from financial institutions and how this is hindering the growth of Pakistan's economy.

-----------

LAHORE -- Only 13% of women in Pakistan own bank accounts, the fourth-lowest proportion in the world.

When she was growing up, Mashal Wali watched her mother, Nasreen Muzaffar, put away a little money every week, storing it in a safe in their home. She would bring it with her when she went to the jamatkhana, a prayer hall for people from the Ismaili subsect of Shiite Islam. There, Muzaffar would contribute the money to a group savings account organized by managers at the adjacent community center near her home in the Gilgit-Baltistan region of northern Pakistan.

The cash Wali's mother saved was leftover pocket money that she had received from her husband for household expenses and food. Muzaffar's contributions, along with savings from other women in her community, went into a joint bank account that she or her neighbors could draw from when they needed money for big expenses. This system helped her save up for personal items as well as gifts for her children, including a bike and a camera.

In Pakistan, community savings systems like the one Muzaffar uses are a mainstay, in part because many people do not have bank accounts of their own.

Pakistan has one of the lowest financial inclusion rates in the world, with 79% of its 231 million people operating outside of the formal banking system, according to the World Bank's Global Findex Database, which tracks the use of financial services. But women are disproportionately on the wrong side of this financial divide: only 13% of Pakistani women have their own bank accounts, compared to 28% of men. In a World Bank survey of over 135 countries and territories, Pakistan finished fourth from the bottom for female financial inclusion. In Asia, it was the third-lowest, after Afghanistan and Yemen. Outside Asia, only South Sudan has a lower level of account ownership by women.

The unbanked deal in cash, borrow from friends and family, and save through community groups built by social networks and trust. It is a system nurtured by communities for generations but rife with local politics and family drama, all of which women must negotiate to make use of informal community savings.

Part of the reason for their lack of access to finance is that roughly 75% of Pakistan's women are not formally employed, according to the World Bank. Many are labeled housewives and homemakers and completely reliant on the incomes of their husbands and other male relatives.

Even formally employed Pakistani women are excluded from banking, with only 16% maintaining their own personal account instead of operating from someone else's account. That compares to an average of 68% of women in developing countries globally who have accounts, according to data from the World Bank.

Pakistan's low rates of financial inclusion for women reflect a societywide issue of gender inequality. The country ranks second-lowest in the world in terms of gender parity, at 145th out of 146 economies in the World Economic Forum's Global Gender Gap Index from 2022. Afghanistan ranks 146th.

The index studies economic participation, education, health and political empowerment. "[In Pakistan], women and men are really standing in very different places," said Shazreh Hussain, an independent social development and gender consultant in Islamabad.

Pakistan's financial gender gap aggravates chronic poverty

https://asia.nikkei.com/Spotlight/The-Big-Story/Pakistan-s-financial-gender-gap-aggravates-chronic-poverty

"The ability for women to independently maintain money, spend money, conduct transactions and get paid for their labor and to control the funds that are theirs, that ability is severely dented or compromised because their engagement with formal banking channels is through men," said Mosharraf Zaidi, founder of Tabadlab, a policy research institute in Islamabad.

In Gilgit, Wali said many women of her mother's generation -- Muzaffar is 51 -- spend their days at home, apart from a weekly trip to the jamatkhana. Community saving there is the easiest choice -- women do not have to make a separate trip to the bank and can trust the financial managers at the nearby community center to handle the details for them.

"Most of the women are illiterate and have never ever been to a school or any learning platform so they don't know anything about how to run normal bank accounts," Wali said, referring to women her mother's age. Education levels are considerably higher for younger generations of women from her area.

The case for improving women's financial inclusion in Pakistan is substantial. The World Bank recognizes women's financial inclusion as a key factor in achieving at least seven out of 17 United Nations Sustainable Development Goals. Women's participation in the labor force in Pakistan has more than doubled during the past three decades, and by some estimates, boosting women's financial inclusion could increase the nation's gross domestic product by 33%.

Getting women involved in finance has also been shown to increase gender equality; a 2022 study by researchers at the University of Groningen found women who are financially included tend to be more independent and have more bargaining power in the household.

Experts say including women in formal financing will help them contribute to Pakistan's economy -- generating activity the cash-strapped country sorely needs. "To make them part of the financial market is the first step towards actually making them part of economic growth," said Fareeha Armughan, a research fellow at the Sustainable Development Policy Institute, a think tank in Islamabad, who specializes in financial inclusion and governance.

Roadblocks to closing the gap

Pakistan is improving access to financial services. The country launched a National Financial Inclusion Strategy in 2015, and the State Bank of Pakistan adopted a Banking on Equality Policy in 2021 to address gendered obstacles to banking. The policy acknowledged how far Pakistan needs to go to close the gender gap in its financial system.

But tackling issues of gender in financial inclusion is a challenge in Pakistan, since reasons for exclusion are often complex -- both social and socio-economic. According to data from Tabadlab, the most common reason cited by Pakistanis for staying out of the formal financial net was insufficient funds. The second most common reason was lack of documentation -- a problem that is frequently faced by women and people from lower socioeconomic backgrounds.

"So much of how we understand Pakistan is actually caught up in a lot of cultural and sociological and societal and political ... analysis," Tabadlab's Zaidi said. "What it ignores is the base foundation for all the dysfunction, which is economic."

In Pakistan, 38% of adults are illiterate and more than 37% of the population lives in poverty, according to Tabadlab. The institute found men are two times more likely than women to be financially included, and residents of urban areas are 1.5 times more likely to be included in formal financing than those of rural areas.

Pakistan's financial gender gap aggravates chronic poverty

https://asia.nikkei.com/Spotlight/The-Big-Story/Pakistan-s-financial-gender-gap-aggravates-chronic-poverty

Armughan said these factors marginalize certain groups in Pakistan, especially women in rural areas, and keep them from seeking out formalized financial services. "Financial exclusion is actually part of a larger phenomenon of service exclusion," she said, adding that service exclusion is an extension of social exclusion.

On the supply side, commercial banks have few incentives to serve women, who are seen as a credit risk if they do not have a steady income stream from a job of their own or if they make up the 1% of Pakistani women who are entrepreneurs.

Strict documentation rules at financial institutions in Pakistan meant to stop money laundering and terror financing can make opening a standard bank account a tedious process for men, and even more so for women, who often are less likely to have official documents, such as land deeds, in their name.

On the demand side, economic marginalization and geographic isolation in rural areas keep both women and men out of formal financing because it is difficult to access banks. Lack of documentation and low literacy rates can also make banking an intimidating and confusing proposition for people from lower social strata. Financial scams in Pakistan often prey on these knowledge gaps among people who are new to formal banking.

Distrust in formal financial systems because of economic uncertainty also plays a role in the scale of Pakistan's informal economy. "[Fewer] people today are confident about savings instruments at banks than they were five years ago, 10 years ago," Zaidi told Nikkei.

Social and religious traditions surrounding gender roles also contribute to the financial gender gap. Men are seen as the primary breadwinners in most families, making it less likely for mothers, wives and daughters to have separate bank accounts. Women in Pakistan are also engaged in unpaid care work at home and in the agricultural sector, keeping them out of the formal financial system because they do not earn salaries in these roles. According to a U.N. Women report published in 2019, Pakistani women spend 11 hours on unpaid care and domestic work for every one hour their male counterparts spend on it.

Simple factors like the distance it takes to walk to a bank or fears of harassment on the way can act as deterrents."[Men] go to offices. They openly walk on the roads, but women don't do this," Wali from Gilgit said, referring to the experiences of women from her mother's generation. These risks contribute to women's preference for saving at the community center, where they already go every week with their families.

Community is key

The pandemic stretched household finances in Pakistan to the breaking point and put informal community financial pools under severe strain. With many unemployed, families had to borrow money to make ends meet, and those debts are starting to fall due.

The country's ongoing economic crisis has also fueled record levels of inflation, which hit 35% in March, making basic necessities considerably more expensive. This has compounded the hardships of those people who were already recovering from financial challenges during the pandemic.

In Molvi Suleman Jat, a village in the district of Thatta in the southern province of Sindh, less than a handful of women have their own bank accounts and most deal entirely in cash-pooling leftover money into a community savings fund used for medical treatments and other emergency expenses. When someone from the group needs cash, group members give from their savings in the form of a loan, deciding on the repayment terms together.

Pakistan's financial gender gap aggravates chronic poverty

https://asia.nikkei.com/Spotlight/The-Big-Story/Pakistan-s-financial-gender-gap-aggravates-chronic-poverty

These types of group saving systems revolve around the idea of social collateral, where the basis of trust is the strength of the ties between group members. In Molvi Suleman Jat, women say they had no conception of saving before a system was started in 2019 through a development program from the Sindh Rural Support Organization funded by the Sindh government. Most women in the village earn through daily labor or by producing and selling local crafts, which allows them to save a minimum of 100 rupees (around 35 cents) per month.

Inez Murray, the CEO of the Financial Alliance for Women, a nonprofit organization focused on women's involvement in financial markets, told Nikkei community savings models are used around the world because of the way they help people in poor communities build up a lump sum. "[It is] a way of putting a barrier between your pocket and somebody else, which is the challenge if you're poor because you just don't have enough resources," she said. "[There are] always competing interests for your money."

People partaking in these systems, however, also often do so because they are excluded from financial services, playing into a cycle of informal borrowing and community financing. Over half of the world's unbanked population is comprised of women, and rates of financial inclusion for women in the developing world have remained largely unchanged for more than a decade despite global efforts to close the gender gap in banking.

Pakistan has targeted women for its national welfare initiative, the Benazir Income Support Programme, through which eligible women receive cash payments through cards issued by the program.

Women-focused programs around the globe have become especially popular in the world of microfinance. Murray says the focus on women in microfinance specifically stems from research that shows women are more trustworthy borrowers than men. "The loan repayment rates in every loan category in every country are better for women," she told Nikkei.

Microfinance is the practice of providing financial services to low-income groups that do not generally have access to them. In her book "Poverty Capital," Ananya Roy describes how the microfinance model, first conceived by Bangladeshi economist Muhammad Yunus, saw women as an important conduit for financing because of their perceived likeliness to use finances for social development, including schooling and investments in the household. The microfinance model, which initially focused on group-based or "solidarity lending," was premised on the idea that social pressure in communal settings encourages women to repay their loans.

Because they became the focus for microfinance loans, however, women also become victims of predatory lending tactics that can increase debt. Murray of the Financial Alliance for Women says such tactics took root when the sector began looking to lower transaction costs to achieve scale and sustainability. "[It became] much more about the loan officer taking the payments back," she said.

Pakistan's microfinance industry has also faced challenges. In 2012, the World Bank found that between 50% and 70% of microfinance loans to women in Pakistan were actually going to male relatives, while women remained responsible for the transaction costs and the stress of repayment. "Women were borrowing money across groups, and it became very difficult to know who was using money at the end of the day," said Roshaneh Zafar, founder of the Kashf Foundation, the first women-focused microfinance institution in Pakistan. "There were men who had also been pipelined the money."

Pakistan's financial gender gap aggravates chronic poverty

https://asia.nikkei.com/Spotlight/The-Big-Story/Pakistan-s-financial-gender-gap-aggravates-chronic-poverty

Zafar said the global financial crisis of 2008, which caused high rates of inflation and led communities to default on loans, pushed the microfinance industry in Pakistan to shift away from group lending. Since then, the uptake of the CNIC national ID card system, the creation of the Credit Information Bureau, and other forms of digitization helped regulate the market and made it easier for lenders to keep track of where the money was going, she said. Still, the financial crisis brought to light the risks of group financing and the continued challenges of female financial access. "Many of us had to rethink and realign models," Zafar said.

Technological solutions

As Pakistan tries to fix its problem of female financial exclusion, the country's state bank has told commercial instructions to step up their efforts to create products and offer services that cater to women, under the 2021 Banking on Equality Policy. Meanwhile, financial technology startups and development organizations are looking at preexisting models of saving to provide clues about how to get women more involved in financial matters.

Potential product revenue from financial services in the women's market in Pakistan is estimated to be around $652 million per year, according to the Women's Financial Inclusion Data Partnership. Many new models addressing female financial inclusion use mobile applications as an alternative to brick-and-mortar banks, which are often difficult for women to access. The State Bank of Pakistan aims to get 20 million digital banking accounts operating for women by the end of this year.

Mobile banking applications like Easypaisa and JazzCash have become increasingly popular across Pakistan and can be used by anyone with a mobile phone. However, there is also a gender gap in phone ownership, with 50% of women owning a cellphone compared to 81% of men, according to the GSMA, an organization that represents mobile telecommunications operators.

Mobile banking options are becoming increasingly popular among Pakistani women, although only half of the female population owns a mobile phone. © AFP/Jiji

In Molvi Suleman Jat, where many of the women are illiterate, dealing in cash is a much better system than mobile banking, which is still an unknown concept. "We lack skills to use smartphones because we never went to school," said Rukiya Jat, a manager for one of the village savings groups. "We are learning. We have the curiosity to be part of the world, so our girls are going to [learn how to] use technology."

Reza Baqir, the former Governor of the State Bank of Pakistan, told Nikkei that none of the conventional explanations related to religion or culture seemed to account for the gender gap he was seeing in Pakistan's finances. Getting commercial banks to see women's accounts as profitable seemed to Baqir the most critical strategy in addressing the gender gap. "It was clearly a case of market failure where the market was not rising up to this opportunity," he said. The State Bank's policy includes a section that requires all banks to create and invest in a specialized banking department for women's products.

Numerous commercial banks in Pakistan -- including Habib Bank Ltd. (HBL), Allied Bank and Bank Alfalah -- have launched women-specific bank accounts to attract more female customers. Accounts like HBL's Nisa Asaan account, which is geared toward low-income women, can be opened with only a national identity card and has no minimum account balance.

Pakistan's financial gender gap aggravates chronic poverty

https://asia.nikkei.com/Spotlight/The-Big-Story/Pakistan-s-financial-gender-gap-aggravates-chronic-poverty

Shazia Gul, head of the Women Market at HBL, said these types of initiatives are meant to help get women financially included by removing the barriers to entry that exist for standard accounts. "We've done that to encourage women and develop a more enabling environment for them so that they're able to become part of the system on easy terms," Gul said. HBL launched its first women's account in 2016. Gul said the Banking on Equality Policy has given an added impetus to focus on women's products and policies. "It's not just about encouraging new accounts for us," Gul said. "It's about activating the existing [accounts] and also encouraging activity."

Some fintech companies in Pakistan have looked to community financing as the first step in getting women banked. Halima Iqbal, the founder of Oraan, a financial services startup, saw business potential in digitizing ballot committees -- a popular form of community savings -- when she returned to Pakistan in 2017 after working in Canada as an investment banker.

Iqbal and her team have helped dozens of women open bank accounts. According to Oraan's research, more than 40% of Pakistanis use the committee system for savings. Iqbal said committees are something women already feel comfortable using, which is why they were willing to try using the digital system. "There's a very deep-rooted cultural, social, religious aspect around it, right, like my mother did it, my grandmother did it," she said.

Oraan thought up a way to digitize committees by creating a platform that could organize the process and give people a trustworthy way to join committees outside of their immediate community. "Very quickly, we started recognizing that people don't necessarily want a better system," Iqbal said. "What they want is access to maybe a larger audience." By expanding on the committee model, Iqbal said Oraan's products seek to decentralize the risk in case certain communities experience a financial shock.

In December, a scam based out of Karachi brought risks of informal financing to life for Mariam Fareed, who'd begun paying into a community savings committee she'd read about in a Facebook group. The group has 35,000 members and in it, women post about their businesses, their homes and their lives.

Fareed started paying 7,500 rupees a month to secure her spot in the committee organized by an active member of the Facebook group, a woman she knew only by name and reputation. After four months, she started reading posts about the organizer, who'd failed to pay out thousands of collective dollars to dozens of members. Fareed got her money back but learned a lesson about blind trust of informal financing. "She didn't give me her details and I guess I also didn't give mine and that's my mistake," Fareed said.

Maham Alavi, who runs a Facebook page with the intention of helping women learn the basics of investing, said this is something she encounters often with women in her network who are only beginning to manage their own finances. Many worry that if they make a mistake investing, they will draw ire from family members, who won't trust them with finances in the future. Alavi said many women in her network lack basic financial literacy or confidence to do anything with their money besides stashing it somewhere in their homes.

Pakistan's financial gender gap aggravates chronic poverty

https://asia.nikkei.com/Spotlight/The-Big-Story/Pakistan-s-financial-gender-gap-aggravates-chronic-poverty

Alavi also tries to encourage women to put their money into investments other than committees, which she sees as less productive than stocks and other financial ventures. Still, if community financing helps women start taking control of their own money, Alavi sees the system as worthwhile because it would give them some protection in unstable living situations. "They just need to have that financial independence that God forbid, if something happens, they have something with them."

Efforts to increase financial inclusion for women in Pakistan have shown signs of progress. From 2017 to 2021, account use by women almost doubled. HBL said the bank's specialized women's accounts now make up 29% of total accounts in branch banking, and 23% of their branchless banking accounts are registered to women.

Wali from Gilgit said there is less desire to use community financing among people from her generation, who are moving away from rural areas to study and work. The 19-year-old has her own bank account, which she uses to pay her accommodation fees for university. "I go to the bank," she said, "so I don't need to use [community savings] because the [other options] are more convenient for me."

Armughan of the Sustainable Development Policy Institute said convenience is one key to getting more women involved. She believes high rates of informal financing should not be seen as a sign that women do not want to be included in formal banking. Instead, it should suggest that formal banking still has a way to go to serve them.

"This market is not designed for [women]," she said. "The products are not tailored for them."

‘Digital Pakistan’ in a coma: What is the cost of the broadband shut down?

https://profit.pakistantoday.com.pk/2023/05/11/digital-pakistan-in-a-coma-what-is-the-cost-of-the-broadband-shut-down/

One of the immediate groups that were affected were gig workers. These are daily workers that earn their money on platforms such as Careem, Foodpanda, and Indrive. These people require stable internet access through mobile phone data to do their jobs. Over these days, Foodpanda and services such as Careem were out of service because their captains and riders had no way of accepting rides/orders or of following maps. To put things in context, there are over 13000 foodpanda and Bykea riders, 30,000 Uber and Careem captains, and around 12,000 Foodpanda home chefs whose daily wages are dependent on broadband data.

Similarly, the shut down also had a serious impact on freelancers. A large number of Pakistanis work for foreign clients remotely on platforms such as Fivver and Upwork providing services ranging from coding to content writing and search engine optimization.

The gig-economy is an emerging sector in Pakistan. Freelancers in the country earned around $400 million in both 2021 and in 2022 which accounts for about 15% of Pakistan’s total $2.6 billion ICT (information-communication-technology) exports.

Almost immediately after the shutdown, both platforms put up signs next to the profiles of Pakistani users saying that the service providers belonged to a country that was experiencing internet outages which could delay their projects. The warning sign was not an exaggeration. A lot of these freelancers depend on broadband data to get their work done. On top of this, the freelancing world is brutal. Clients are very picky and small interruptions can very quickly sour client relationships that take years to build sometimes.

If this were not enough, the dream of a Digital Pakistan took another blow in the form of the Point-of-Sale machines also being out of service. A lot of the terminals you see at stores that are used to accept card payments come with in-built sims that connect them to the internet. As a result, Pakistan’s retail and grocery sector was operating entirely on cash. Even the country’s Federal Board of Revenue uses the data from these machines for tax calculation purposes.

Point of Sale (POS) machines, often known as debit/credit card machines, use sims to establish a network connection and make digital payments. The severance of mobile internet signals has rendered these machines temporarily obsolete, limiting everyone to cash payments only.

Reuters reported that Pakistan’s main digital payment systems fell by around 50% the day after former Prime Minister Imran Khan’s arrest. Data shared with Reuters by 1LINK on POS through its platform showed international payment card transactions were down on Wednesday by 45% in volume, from a daily average of 127,000 during the week of May 1 to 7 to approximately 68,000 on May 10. Ali Habib, spokesperson at HBL, Pakistan’s largest bank, said that it had seen a decline of 60% in the throughput of the POS machines.

Laying the digital foundations for a brighter future

https://dailytimes.com.pk/1095721/laying-the-digital-foundations-for-a-brighter-future/

by Khurram Sultan

The Government of Pakistan has launched the Smart Village Pakistan project with the support of Huawei to overcome the extreme disparity between the urban and rural development indicators. The Smart Village project aims to achieve digital transformation in remote rural areas by closing the gap in access to technology and services between urban and rural areas – a transformation that is made possible through Huawei’s expertise and expansion of wireless broadband network coverage.

The first village to experience the digital transformation is the Gokina Smart Village, a small hamlet near Islamabad. There, Huawei provides cutting edge technical solutions to connect the unconnected, allowing partners in education and health to serve the previously underserved community.

The Smart Village Pakistan project aims to digitally transform remote and rural communities by connecting them and empowering the citizens with better access to a range of digital services that can meaningfully improve their wellbeing and livelihoods in accordance with the government’s vision of Digital Pakistan. Reduced inequality will lead to improved well-being and access to better jobs through digital services. This approach involves a new design and implementation framework that is demand-driven, user-centric, flexible, and is focused on sustainability, scalability, and multi-sector collaboration.

Huawei continues to be the leader in Pakistan in expanding outreach in rural areas under the broader Huawei TECH4ALL commitment to enable an inclusive and sustainable digital world. Aligned with the UN SDGs and Huawei’s vision and mission, TECH4ALL is a long-term digital inclusion initiative and action plan to innovating technologies and solutions that make the world a more inclusive and sustainable space for all.

Approximately half the world population is digitally connected while the other half is not, a division that has implications that became glaring apparent during the global pandemic when digital networks and access to the internet meant continued access to fundamental rights and critical services like health and education.

TeleTaleem is a social enterprise focused on enhancing quality of education services at the grassroots level, through innovative use of technology. While TeleTaleem has reached a good mix of users in urban and rural settings – reaching out to 60 different districts across all four provinces and the AJK, covering 4,000+ schools and directly impacting skillset of more than 6,000 teachers and 1,000,000+ children, one of its proudest accomplishments is the recent partnership with Huawei and the International Telecommunication Union (ITU) under the Smart Village Program.

Upon visiting the school in Gokina, TeleTaleem discovered a pressing need for science teachers, particularly for students in grades 8, 9, and 10. Specializing in the design and delivery of e-learning systems and services, using a variety of delivery mechanisms and blended learning platforms, TeleTaleem has implemented multiple interventions, covering a broad spectrum of primary to secondary school systems, teacher education and training institutions in both public and private sectors.

The solution for Gokina was TeleTaleem’s Online Teaching Model, which provides the school with two digital classrooms equipped with internet connectivity from Jazz and power backup systems. Through this setup, the school was connected with specialist science teachers based at TeleTaleem. Now, the students in Gokina are benefitting from daily science classes, including subjects like chemistry and biology, along with regular assessments of their learning activities.

USF Approves Rs. 21 Billion for New Optical Fiber and Broadband Projects

https://propakistani.pk/2022/09/25/usf-approves-rs-21-billion-for-new-optical-fiber-and-broadband-projects/

The Universal Service Fund (USF) Board has approved the award of 10 contracts worth approximately Rs. 21 billion for the unserved and under-served communities of Baluchistan, Punjab, Sindh, and Khyber Pakhtunkhwa (KP).

The high-speed mobile broadband projects, highways and motorways projects, and optical fiber cable projects will provide 4G LTE connectivity and backhaul connectivity to around 3.5 million people by connecting 187 Union Councils (UCs) with 1,554 kilometers (kms) of optical fiber cable and provide seamless connectivity to 622 km of unserved road segments on M-8 motorway and N-35 highway.

Additional Secretary (Incharge) IT & Telecommunication and Chairman USF Board Mohsin Mushtaq Chandna chaired the 83rd Board of Directors meeting of USF on Thursday.

While addressing the meeting, Chandna said that USF has delivered a record productive performance in the past 4 years by contracting 79 projects worth approximately Rs. 62.7 billion in subsidy. This is a testament to our absolute commitment to improving the lives and livelihoods of the unserved and underserved communities of Pakistan.

He also highlighted the importance of infrastructure, affordability, and accessibility of the internet and pledged to work with all stakeholders to achieve the vision of Digital Pakistan.

USF Chief Executive Officer Haaris Mahmood Chaudhary apprised the Board members of the progress of the current projects and the restoration of the flood-affected USF network. He said that these projects will empower around 3.3 million people living in far-flung and backward areas across Pakistan, enabling them to access e-services across various spheres, ranging from financial services like banking and loans to accessibility towards various government services and benefits.

According to the details, the Board approved the award of 5 high-speed mobile broadband contracts worth approximately Rs. 7.1 billion for providing 4G LTE services in the rural and remote districts of Punjab, Sindh, and Balochistan. These projects will benefit people living in 262 unserved muazas of Dera Ghazi Khan, Layyah, Muzaffargarh, Multan, and Rajanpur districts in Punjab, Jamshoro in Sindh, and Barkhan, Musakhel, Sherani, and Sibi in Balochistan covering an approximate unserved area of 12,784.91 sq. km.

Furthermore, the Board also approved the award of two high-speed mobile broadband projects for National Highways and Motorways worth Rs. 6 billion for providing 4G LTE services to commuters on unserved road segments of 622.68 km on M-8 motorway and N-35 highway respectively.

Similarly, the USF Board also approved the award of three optical fiber cable projects worth approximately Rs. 7.7 billion for providing backhaul connectivity to 187 Union Councils (UCs) of Punjab and KP. Under these projects, USF will deploy a total of 1,554 km of optical fiber cable that will benefit over 3.3 million people in the districts of Attock, Sheikhupura, and Nankana Sahib in Punjab and Bannu and Lakki Marwat in KP. These projects are designed to connect 684 educational institutions, 223 government offices, and 268 health institutions along with mandatory connectivity of 408 BTS towers.

Public cloud services on the rise in Pakistan

Cloud computing market in country expected to reach $1.5b this year

https://tribune.com.pk/story/2406357/public-cloud-services-on-the-rise-in-pakistan

According to a report of IDC, public cloud spending in Asia-Pacific excluding Japan (APeJ) is expected to grow at a compound annual growth rate (CAGR) of 25.5% from 2019 to 2024, reaching $124.5 billion in 2024.

Another report of Gartner suggests that the public cloud services market in the Asia-Pacific region will grow by 23.7% in 2021 and reach $124.6 billion, up from $100.8 billion in 2020.

In Pakistan, the adoption of public cloud services is also on the rise. Allied Market Research, in its report, says the cloud computing market in Pakistan is expected to reach $1.5 billion by 2023, growing at a CAGR of 19.1% from 2017 to 2023.

“These numbers highlight the increasing importance of public cloud for businesses in Asia and Pakistan, as they embrace digital transformation and seek to leverage the benefits of cloud computing to enhance their competitiveness and drive growth,” remarked Azam.

Cloud computing provides organistions with the ability to rapidly scale resources up or down, as needed, allowing them to handle changes in demand more effectively.

According to an IDC study, organisations that use cloud computing are able to handle 2.5 times more application workloads than those that rely on the traditional IT infrastructure.

Talking about the security of public cloud, Azam cited a Forrester Research report which said that 80% of security breaches involving the public cloud infrastructure are caused by customer misconfiguration or mistakes.

“This shows that while cloud providers have strong security measures in place, organisations also have a responsibility to ensure their data is secure in the cloud,” he added.

Overall, the importance of public cloud services for businesses in Asia and Pakistan cannot be overstated, as it provides them with the ability to innovate, collaborate, and scale with ease, while reducing costs and improving security and reliability.

“Public cloud offers a pay-as-you-go model and the ability to scale resources up or down, as needed, which makes it easier for organisations to handle fluctuating workloads without having to invest in additional hardware or infrastructure. In contrast, private cloud requires organisations to invest in and maintain their own infrastructure which can be costly. Private cloud offers more control over data and infrastructure, which can be beneficial for organisations with strict security requirements.”

NADRA launches Nishan Pakistan platform, lets startups leverage digital identity stack | Biometric Update

https://www.biometricupdate.com/202305/nadra-launches-nishan-pakistan-platform-lets-startups-leverage-digital-identity-stack

The National Database and Registration Authority (NADRA) has launched the Beta version of Nishan Pakistan, a platform to enable small and medium sized businesses in the country make the most of its digital ID stack.

NADRA Chairman Tariq Malik said in a tweet that Nishan Pakistan is a game-changer platform designed to empower commercial startups and young entrepreneurs with secure and contactless biometric verification through secure data sharing with NADRA.

He said the platform, which offers a world of endless possibilities and a plethora of use cases for businesses including customer identification through biometrics, is the first of its kind online, secure and open digital identity authentication platform in the country.

Malik added that the platform offers an API gateway and a cutting-edge sandbox that enables a smooth integration with other systems and will provide a set of services that will help businesses with “a seamless, consistent and connected experience,” and also contribute to ongoing efforts of making Pakistan a truly digital nation.

The official said in another message that the novelty will set the stage for the kind of market-creating innovation that ignites “the economic engine of a country, creates jobs and augments profits that fund public services and promote change culture in the society.”

Nishan Pakistan has been rolled out for user acceptance testing and NADRA is looking out for feedback to improve the functionality of the platform and also help in its plans of creating a strong digital ID system.

Subscriptions to the platform are opened and interested businesses can submit applications and wait for the approval process to be completed in 10-15 days, according to a promotional video.

In April, NADRA announced the market launch of the automated fingerprint identification system (AFIS)) it developed domestically.

Super Fast Gigabit Fiber Internet is Coming to 11 Cities in Pakistan Soon

https://propakistani.pk/2023/06/07/super-fast-gigabit-fiber-internet-is-coming-to-11-cities-in-pakistan-soon/

Pakistan is about to get ultra-fast gigabit fiber internet in eleven cities soon, as per government documents available with ProPakistani.

This document highlights the Public Sector Development Project (PDSP) budget during the period of 2022-2024. It includes a summary of current ongoing projects, future projects, and more under the Ministry of Planning, Development, and Special Initiatives.

Under the Information Technology and Telecom Division, it highlights a new scheme for a project that will expand Gigabit Passive Optical Network (GPON) Fiber to the Home (FTTH) services to eleven cities.

In simpler words, super fast gigabit internet is coming to more cities soon, as mentioned earlier. The project’s approval status is still “under process”, so it will probably be a while before it sees the light of day.

The government has approved a cost of Rs. 800 million and there is no foreign aid on this particular project. An additional Rs. 50 million will be allocated to this project during the course of 2023-2024.

Other Development Projects

The IT section of the document also highlights dozens of other projects the govt is working on at the moment, such as 4 more knowledge parks, a technology park development project, an online recruitment system for FPSC, smart offices for Federal Ministries and Departments, expansion of broadband services in Kashmir and Gilgit, and much more.

Dear Sir

I hope you are doing well , Sir pls check the latest news , China has built its own version of quantum computer which is more advance and much faster than a super computer . This quantum computer developed and designed by China can solve complex and big problems within few seconds or even less than seconds which takes the super computer to solve in 5 years . Sir it also says that it can solve artificial intelligence related tasks in few seconds meaning that it can solve such AI related tasks millions times faster . Pls check this

A quantum computer, Juizhang, built by a team led by Pan Jianwei, has claimed that it can process artificial intelligence (AI) related tasks 180 million times faster, the South China Morning Post reported. Jianwei is popularly known as the "father of quantum" in the country.

Sir can you pls make a blog about it ?

Thanks

Chinese firm starts to lay 16,000-km-long fibre-optic cable in Pakistan

https://www.thenews.com.pk/print/1072079-chinese-firm-starts-to-lay-16-000-km-long-fibre-optic-cable

This was stated by Tony Lee, Chief Executive Officer of Sunwalk Pvt Limited, during a ceremony held in Islamabad. This Chinese company had already invested $5 million in Pakistan, and now planning to invest $100 million for laying optical fiber in other parts after getting Right of Way (ROW) from different public sector departments.

Tony Lee said Sunwalk is focusing on fast deployment and concentrating on quality according to the ITU-T Standards. “We are always committed to the best services in Pakistan”, he said.

Two months ago, Sunwalk Group Chairman Hou Xing Wang told Federal Minister for IT and Telecom Aminul Haque in a meeting Sunwalk Group will soon start laying fiber cable across the country with substantial investment.

According to an official statement about the project, Ms Afshaan Malik, Chief Business Officer of Sunwalk Group Pakistan, said keeping in view Pak-China long-term strategic relationships, Sunwalk has fulfilled its promise by initiating the national fiber backbone project. Sunwalk is committed to providing optic cable to the people of Pakistan, she said.

In this connection, groundbreaking of Phase-1 (Islamabad to Multan) to provide nationwide fiber backbone was done on Thursday. Afshaan further said Sunwalk is in the process of getting ROW from government departments. After getting that $100 million will be invested, she said.

Aatif Awan

@aatif_awan

1/ Starting from Pakistan's heartland & now expanding to the world's farm (Brazil), what a journey it's been for the

@FarmdarOfficial

team. Congrats to them on launching AgromAI, a fintech venture in Brazil that leverages AI & geospatial data to create agri financial solutions

https://twitter.com/aatif_awan/status/1676570789913542657?s=20

-----------------

Aatif Awan

@aatif_awan

2/ Think insurers having highly accurate, individual farm-level intelligence to underwrite crop insurance. Imagine banks using the same information to provide credit to farmers. At $170+ billion, Brazil is one of the top agri markets. Crop insurance alone is at ~ $2B annually

-------------

Aatif Awan

@aatif_awan

3/ What's amazing is that the tech is built in Pakistan by Pakistani product and engineering talent. And it's finding traction in one of the largest markets for agritech

------------------

Aatif Awan

@aatif_awan

4/ Really proud of the Farmdar founders

@MBukhari80

,

@MujiManghi

, Ibrahim Akbar Bokhari and the entire Farmdar team on this huge milestone. Congrats team!

We hope this will inspire many other "Made in Pakistan, For the World" products

-----------

Pakistan’s Farmdar Has Just Launched a New FinTech Startup in Brazil

https://www.techjuice.pk/pakistans-farmdar-has-just-launched-a-new-fintech-startup-in-brazil/

https://twitter.com/FarmdarOfficial/status/1676487324614402050?s=20

Named ‘AgromAI’, Farmdar’s fintech startup in Brazil will use artificial intelligence (AI) and geospatial data to provide financial services

Pakistan based agri-tech startup ‘Farmdar’ has just announced the launch of its new fintech venture. What’s unique about this new expansion is the fact that it is based in Brazil; a new industry in a new country, sounds exciting right?

Named ‘AgromAI’, Farmdar’s new fintech startup will utilize artificial intelligence (AI) and geospatial data in order to provide financial services, but how would it do so?

Well, according to Farmdar co-founder and CEO Muzaffar Manghi, Latin America is going through a severe climate change, therefore both rainfall and temperatures are evolving at a massive speed, putting both insurers and agricultural business at risk.

AgromAI, using its geospatial data and artificial intelligence systems, will make sure that financial institutions and insurers can avoid and respond to these risks. Having individual farm-level intelligence, these insurers and institutions will have the best insurance risk management in place, allowing an increased productivity and growth in Brazil’s agricultural sector.

“Pakistani technology will be used by some of the largest businesses in the world, and with more developed markets as a stomping ground,” said CEO Muzaffar Manghi while talking about the new startup.

“We are extremely proud to export our artificial intelligence and data-backed products developed solely by Pakistani engineers. This is a testament to the innovation of Pakistani talent and their potential to make a contribution to the global agritech industry,” said Farmdar in its official press release.

Agriculture makes up for a large part of the Brazilian economy, with the country being the world’s third-largest exporter of agricultural products and an agricultural production valued at $170+ billion, whereas Brazil’s crop insurance market, the primary target for AgromAI, accounts for over $9+ billion annually.

How the mobile phone is transforming Pakistan - Newspaper - DAWN.COM

https://www.dawn.com/news/1448782

How are we navigating our daily lives, connecting with our surroundings, equipped with the mobile phone?

Faiza Shah Published December 2, 2018

Mehreen Kashif from Larkana, for example, manages a business of hand-embroidered apparel and bed linen without leaving her home. It has been four years since she launched her work-from-home enterprise through a Facebook page and then contacting clients through WhatsApp.

“Women are not allowed to leave home here,” she explains. Owning a mobile phone has been a game-changer, though, as she has been able to expand her business over only four years and that, too, countrywide. Most of her clients are from Punjab, where she also orders fabric from. She has it shipped from Al Karam textile mills in Faisalabad. She simply puts up new designs and items on her WhatsApp status and the orders from her phone contacts pour in. She estimates about 4,000 repeat customers but also claims that they are “unlimited” and “it is almost getting hard to keep up with the orders.”

Mehreen caters to customised orders as well. She has 30 women working for her, and has provided two of them with mobile phones as, “it is easier to share pictures of the designs they work with.” Her effort is to seek out embroiderers with skill but also those who are truly in need of money. And this is a driving force behind managing her business; the ability to employ women who have talent but are house-bound under the dictates of rural traditions.

“They just come to my house for work,” she says of her employees. “The phone has facilitated us living in such an area where women are not allowed to leave their houses. It has helped me because I also do not have permission to go out.”

A similar story is echoed by Salma Ilyas, who runs a kitchen business in Karachi to provide home-cooked meals to “a young professional class”. Mother to four young ones, her husband owned a small business of selling paper. One fine day, the business got wrapped up as the owner of the building housing the paper shop decided to remove all businessmen from the building. With no backup plan, with no storage space for the bundles of paper already bought in wholesale, the Ilyases were in trouble.

“One day, I just cooked achaar gosht and put up pictures on my Facebook wall,” narrates Salma. “People started liking the photos and asked how much for a plate. That sparked an idea to sell what I cook. That week I made almost as much as my husband would make every week in his paper business.”

Things suddenly changed financially for the Ilyases as Salma dragged the family out of its quagmire. With some savings, she upgraded her cooking range, bought better utensils, and went full-time. Her husband now receives orders on WhatsApp and handles the food delivery component of the business. The paper from the old business was sold onwards to someone else. And as Salma puts it, her marriage and domestic harmony seems to be at an all-time high because of WhatsApp.

What is interesting is how travel and restaurant deliveries — 31 percent and 24 percent consumers respectively purchasing within the category — are driving the growth for the evolving mobile industry in Pakistan.”

As with the Ilyases, the mobile phone has brought together the service provider and client, almost eliminating the middleman entirely. Business cards used to be a thing of yesteryear, now it’s the WhatsApp number. The service provider, such as an electrician, a cook, or a car mechanic, gives their mobile number to clients along with a fair bit of reliability. As clients have a mobile number of the electrician or AC repairman, they can catch a hold of him pretty much anytime during working hours. In other words, phones have broadened opportunities for recreation and business alike.

Digital public infrastructure is transforming lives in Pakistan. Here's how

https://www.weforum.org/agenda/2024/07/digital-public-infrastructure-is-transforming-lives-in-pakistan/

Likewise, NADRA's role in the RAAST payment system - a State Bank of Pakistan initiative – highlights how DPI can transform financial transactions. RAAST, an interoperable instant payment system, utilizes NADRA's identity authentication processes to offer secure, swift KYC-compliant financial transactions across various platforms, thereby democratizing access to digital payments for millions.

Additionally, Pakistan's DPI framework has also proven instrumental in managing crises, such as the COVID-19 pandemic. Within days of initiating the lockdown, Pakistan's federal authorities announced unconditional cash transfers. The government provided approximately $75 per household, sufficient to purchase three months' worth of food staples to 12 million vulnerable households.

The targeted response, facilitated by the robust digital ID infrastructure provided by NADRA, resonates strongly with the United Nations-based Better Than Cash Alliance’s 10-point action plan. This plan urges digitizing social benefits and providing women with Digital IDs, mobile phones, and internet access to advance financial equality.

The same approach is endorsed by a recent report on the Benazir Income Support Program (BISP), which highlights significant advancements in Pakistan’s digital delivery system.

These significant opportunities need to be informed and designed with guardrails to ensure that the deployment of DPI is safe, responsible, and leveraged for inclusive societies. The Universal Safeguards for DPI initiative, and the UN Principles for Responsible Digital Payments aim to create a practical framework for countries implementing such initiatives. This initiative identifies potential risks in global DPI deployments, providing valuable insights to inform the design and implementation of future safeguards.

Digital public infrastructure is transforming lives in Pakistan. Here's how

https://www.weforum.org/agenda/2024/07/digital-public-infrastructure-is-transforming-lives-in-pakistan/

Digital public infrastructure (DPI) initiatives in Pakistan are enabling financial inclusion and empowering citizens, especially in underserved areas.

Pakistan's National Database & Registration Authority is responsible for a digital identity system, which facilitates transactions for citizens.

Maintaining the safe and responsible deployment of DPI requires political commitment, robust legal frameworks, and ethical principles.

History teaches us that even the simplest technological innovations can have the most profound consequences for society. From the railways to the internet, technologies have reshaped our lives. Today, digital public infrastructure (DPI) represents such a determining investment. In the case of Pakistan, the country has demonstrated its commitment towards digital transformation, marked by interventions in 2022.

On a scorching day with temperatures soaring to 42 degrees, Manzoora, a mother from the flood-stricken district of Shaheed Benazirabad, rural Sindh, Pakistan, made a significant leap: she withdrew cash from her own bank account for the very first time. This milestone was made possible through a mobile cash transfer programme initiated by the Sindh government, which partnered with digital service providers to empower citizens like Manzoora. This is just one example of how DPI is changing lives of millions of Pakistanis.

Pakistan's digital transformation

At the heart of Pakistan's digital transformation is the National Database and Registration Authority (NADRA), established to overhaul the country's identity systems. This was a foundational change, positioning Pakistan among a select group of nations equipped to manage comprehensive digital identities for over 240 million citizens. The NADRA-issued Computerized National Identity Card (CNIC) is now a standard feature in every adult Pakistani's life, facilitating a range of routine tasks such as opening bank accounts, purchasing airline tickets, acquiring driver’s licenses, and qualifying for social protection, thereby ensuring seamless identity authentication for every citizen.

Within four years of launching the Benazir Income Support Programme (BISP) – a social protection initiative to alleviate poverty – CNIC issuance to adults increased by 72%. Despite its head-start to similar digital identity (ID) initiatives in other countries, optimal use of NADRA's digital database remains limited to only few ministries, department, agencies, and regulated businesses.

The crucial role of political support and legislation

The success of DPI hinges on enduring political commitment and robust legal frameworks that transcend electoral cycles. While the concept of citizen registration was embedded in Pakistan’s 1973 constitution, the integration of various national databases through the NADRA Ordinance 2000 and subsequent legislative enhancements in 2012 have been critical.

Pakistan's digital initiatives

Pakistan's journey toward effective DPI is characterized by the rollout of significant digital initiatives, such as, Contactless Biometric Verification App, Nishan Pakistan, and Pakistan Digital Census. While these prioritize long-term benefits, it is essential to achieve short-term wins to maintain engagement and support, preventing loss of momentum due to shifts in leadership or political will.

For instance, by integrating digital IDs with banking and telco services, the Asaan Mobile Account (AMA) scheme launched in December 2021, within the span of two years secured more than 10 million mobile accounts, with around 40% being women-owned.

Digital public infrastructure is transforming lives in Pakistan. Here's how

https://www.weforum.org/agenda/2024/07/digital-public-infrastructure-is-transforming-lives-in-pakistan/

Digital public infrastructure (DPI) initiatives in Pakistan are enabling financial inclusion and empowering citizens, especially in underserved areas.

Pakistan's National Database & Registration Authority is responsible for a digital identity system, which facilitates transactions for citizens.

Maintaining the safe and responsible deployment of DPI requires political commitment, robust legal frameworks, and ethical principles.

History teaches us that even the simplest technological innovations can have the most profound consequences for society. From the railways to the internet, technologies have reshaped our lives. Today, digital public infrastructure (DPI) represents such a determining investment. In the case of Pakistan, the country has demonstrated its commitment towards digital transformation, marked by interventions in 2022.

On a scorching day with temperatures soaring to 42 degrees, Manzoora, a mother from the flood-stricken district of Shaheed Benazirabad, rural Sindh, Pakistan, made a significant leap: she withdrew cash from her own bank account for the very first time. This milestone was made possible through a mobile cash transfer programme initiated by the Sindh government, which partnered with digital service providers to empower citizens like Manzoora. This is just one example of how DPI is changing lives of millions of Pakistanis.

Pakistan's digital transformation

At the heart of Pakistan's digital transformation is the National Database and Registration Authority (NADRA), established to overhaul the country's identity systems. This was a foundational change, positioning Pakistan among a select group of nations equipped to manage comprehensive digital identities for over 240 million citizens. The NADRA-issued Computerized National Identity Card (CNIC) is now a standard feature in every adult Pakistani's life, facilitating a range of routine tasks such as opening bank accounts, purchasing airline tickets, acquiring driver’s licenses, and qualifying for social protection, thereby ensuring seamless identity authentication for every citizen.

Within four years of launching the Benazir Income Support Programme (BISP) – a social protection initiative to alleviate poverty – CNIC issuance to adults increased by 72%. Despite its head-start to similar digital identity (ID) initiatives in other countries, optimal use of NADRA's digital database remains limited to only few ministries, department, agencies, and regulated businesses.

The crucial role of political support and legislation

The success of DPI hinges on enduring political commitment and robust legal frameworks that transcend electoral cycles. While the concept of citizen registration was embedded in Pakistan’s 1973 constitution, the integration of various national databases through the NADRA Ordinance 2000 and subsequent legislative enhancements in 2012 have been critical.

Pakistan's digital initiatives

Pakistan's journey toward effective DPI is characterized by the rollout of significant digital initiatives, such as, Contactless Biometric Verification App, Nishan Pakistan, and Pakistan Digital Census. While these prioritize long-term benefits, it is essential to achieve short-term wins to maintain engagement and support, preventing loss of momentum due to shifts in leadership or political will.

For instance, by integrating digital IDs with banking and telco services, the Asaan Mobile Account (AMA) scheme launched in December 2021, within the span of two years secured more than 10 million mobile accounts, with around 40% being women-owned.

Digital public infrastructure is transforming lives in Pakistan. Here's how

https://www.weforum.org/agenda/2024/07/digital-public-infrastructure-is-transforming-lives-in-pakistan/

Likewise, NADRA's role in the RAAST payment system - a State Bank of Pakistan initiative – highlights how DPI can transform financial transactions. RAAST, an interoperable instant payment system, utilizes NADRA's identity authentication processes to offer secure, swift KYC-compliant financial transactions across various platforms, thereby democratizing access to digital payments for millions.

Additionally, Pakistan's DPI framework has also proven instrumental in managing crises, such as the COVID-19 pandemic. Within days of initiating the lockdown, Pakistan's federal authorities announced unconditional cash transfers. The government provided approximately $75 per household, sufficient to purchase three months' worth of food staples to 12 million vulnerable households.

The targeted response, facilitated by the robust digital ID infrastructure provided by NADRA, resonates strongly with the United Nations-based Better Than Cash Alliance’s 10-point action plan. This plan urges digitizing social benefits and providing women with Digital IDs, mobile phones, and internet access to advance financial equality.

The same approach is endorsed by a recent report on the Benazir Income Support Program (BISP), which highlights significant advancements in Pakistan’s digital delivery system.

These significant opportunities need to be informed and designed with guardrails to ensure that the deployment of DPI is safe, responsible, and leveraged for inclusive societies. The Universal Safeguards for DPI initiative, and the UN Principles for Responsible Digital Payments aim to create a practical framework for countries implementing such initiatives. This initiative identifies potential risks in global DPI deployments, providing valuable insights to inform the design and implementation of future safeguards.

For instance, in Pakistan, NADRA's data sharing follows strict parliamentary processes. In national security cases, the crisis management cell within the Ministry of the Interior responsible for evaluation and requests of specific data fields. These standard operating procedures ensure case-by-case data sharing, a clear paper trail, and accountability to NADRA's board.

The future of Pakistan's digital economy

The potential of DPI to transform Pakistan's economy and society is immense. With projections suggesting that wholesale adoption of digital payments could boost GDP by up to 7%.

Looking ahead, Pakistan is set to launch several ambitious DPI initiatives, including expanding the RAAST payment system, implementing a nationwide digital health records system, and launching a blockchain-based land registry. These projects promise to drive efficiency and transparency across multiple sectors, positioning Pakistan as a pioneer in the global digital landscape.

Digital public infrastructure is transforming lives in Pakistan. Here's how

https://www.weforum.org/agenda/2024/07/digital-public-infrastructure-is-transforming-lives-in-pakistan/

Likewise, NADRA's role in the RAAST payment system - a State Bank of Pakistan initiative – highlights how DPI can transform financial transactions. RAAST, an interoperable instant payment system, utilizes NADRA's identity authentication processes to offer secure, swift KYC-compliant financial transactions across various platforms, thereby democratizing access to digital payments for millions.

Additionally, Pakistan's DPI framework has also proven instrumental in managing crises, such as the COVID-19 pandemic. Within days of initiating the lockdown, Pakistan's federal authorities announced unconditional cash transfers. The government provided approximately $75 per household, sufficient to purchase three months' worth of food staples to 12 million vulnerable households.

The targeted response, facilitated by the robust digital ID infrastructure provided by NADRA, resonates strongly with the United Nations-based Better Than Cash Alliance’s 10-point action plan. This plan urges digitizing social benefits and providing women with Digital IDs, mobile phones, and internet access to advance financial equality.

The same approach is endorsed by a recent report on the Benazir Income Support Program (BISP), which highlights significant advancements in Pakistan’s digital delivery system.

These significant opportunities need to be informed and designed with guardrails to ensure that the deployment of DPI is safe, responsible, and leveraged for inclusive societies. The Universal Safeguards for DPI initiative, and the UN Principles for Responsible Digital Payments aim to create a practical framework for countries implementing such initiatives. This initiative identifies potential risks in global DPI deployments, providing valuable insights to inform the design and implementation of future safeguards.

For instance, in Pakistan, NADRA's data sharing follows strict parliamentary processes. In national security cases, the crisis management cell within the Ministry of the Interior responsible for evaluation and requests of specific data fields. These standard operating procedures ensure case-by-case data sharing, a clear paper trail, and accountability to NADRA's board.

The future of Pakistan's digital economy

The potential of DPI to transform Pakistan's economy and society is immense. With projections suggesting that wholesale adoption of digital payments could boost GDP by up to 7%.

Looking ahead, Pakistan is set to launch several ambitious DPI initiatives, including expanding the RAAST payment system, implementing a nationwide digital health records system, and launching a blockchain-based land registry. These projects promise to drive efficiency and transparency across multiple sectors, positioning Pakistan as a pioneer in the global digital landscape.

USF Invested Rs. 79 Billion in Rural Telecom Expansion in Last Five Years

https://propakistani.pk/2024/07/30/usf-invested-rs-79-billion-in-rural-telecom-expansion-in-last-five-years/

The Universal Service Fund (USF) has launched 85 projects worth Rs. 79.1 billion in the last five years to expand telecommunication services to rural, remote, and underserved areas of Pakistan.

According to a document seen by ProPakistani, in the last five years, USF has focused on providing 3G/4G services, launching 67 projects worth Rs. 51.4 billion. This effort has resulted in the installation of 2,600 telecom towers, covering 922 kilometers of highways and motorways, and connecting 27 tourist destinations across Pakistan.

USF’s efforts have made a significant impact, serving 24.2 million people in over 12,600 mauzas. The organization has also completed 18 optical fiber cable projects worth Rs. 27.7 billion, laying 10,260 kilometers of fiber to connect more than 926 union councils and towns.

According to the USF, the expansion of telecommunication services has far-reaching implications for the country, enabling greater connectivity and access to information. USF’s initiatives have bridged the digital divide, bringing modern communication services to previously unserved and underserved areas.

Through its projects, USF aims to promote digital inclusion and socio-economic development in Pakistan. By providing reliable and high-speed internet access, USF is empowering communities and driving economic growth in the country’s most remote and rural areas.

This e-banking platform is narrowing Pakistan's financial gap | World Economic Forum

https://www.weforum.org/videos/edisonalliance-pakistan/

---------------

https://www.sbp.org.pk/Finc/AMAscheme.html

Through the Asaan Mobile Account (AMA) platform, any Pakistani holding a valid CNIC can open a bank account digitally in any AMA participating bank, from anywhere, at any time by using the SIM of any mobile operator. The scheme allows individuals to access AMA platform using a short code i.e *2262# and make transactions, through their basic/smart mobile phone without the need for internet connectivity.